Daily review of urea: New orders in the market are traded cautiously, urea prices are adjusted downward (November 27)

China Urea Price Index:

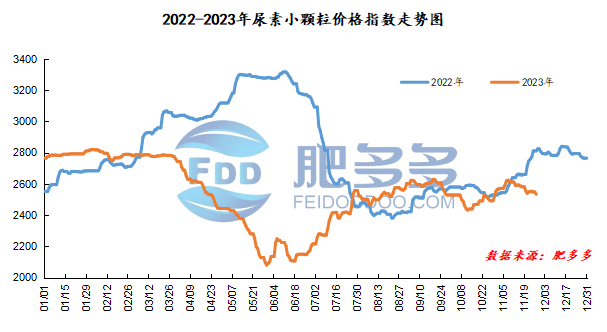

According to Feiduo data, the urea small pellet price index on November 27 was 2,533.91, down 14.55 from last Friday, down 0.57% month-on-month, and down 9.87% year-on-year.

Urea futures market:

Today, the opening price of the Urea UR2401 contract is 2256, the highest price is 2306, the lowest price is 2230, the settlement price is 2274, and the closing price is 2285. The closing price is 9% higher than the settlement price of the previous trading day, and the month-on-month increase is 0.40%. The fluctuation range of the whole day is 2230-2306; the basis of the 01 contract in Shandong is 125; the 01 contract has reduced its position by 8652 lots today, and so far, the position is 201603 lots.

Spot market analysis:

Today, China's urea prices showed a downward trend. Affected by the decline in futures prices in the previous period, the current market sentiment has cooled significantly, and new orders have been traded in general.

Specifically, prices in Northeast China have stabilized at 2,550 - 2,600 yuan/ton. Prices in North China fell to 2,340 - 2,610 yuan/ton. Prices in Northwest China fell to 2,470 - 2,480 yuan/ton. Prices in Southwest China are stable at 2,520 - 2,800 yuan/ton. Prices in East China fell to 2,410 - 2,460 yuan/ton. The price of small and medium-sized particles in Central China fell to 2,430 - 2,650 yuan/ton, and the price of large particles stabilized at 2,580 - 2,660 yuan/ton. Prices in South China fell to 2,640 - 2,660 yuan/ton.

Market outlook forecast:

In terms of factories, the quotations of mainstream companies continue to remain firm supported by pending orders. Some factories are affected by the gradual decrease in pending orders, and prices are loosened and adjusted downward. In terms of supply, Nissan still maintains a high level during the company's shipments and continuous accumulation of warehouses. This week, some pneumatic devices were stopped, and the specific parking cycle is still a key point affecting supply. On the market side, after several consecutive days of rising prices in the second half of last week, industry operators have gradually become afraid of heights. The market trading atmosphere has weakened, and the overall pace of purchasing has slowed down. On the demand side, agricultural demand is still in a gap period. There are signs of improving the start-up of industrial compound fertilizer companies, and their ability to consume urea has become stronger. In addition, there is an intention to start short reserves. Some traders are waiting to enter the market at a timely and appropriate time to get goods. However, the resistance to high prices in the market still exists. Affected by the policy of ensuring supply and stabilizing prices, downstream chasing high prices is limited, and some industry operators have entered a short-term wait-and-see mood.

On the whole, the urea market has a positive impact on production cuts, negative impact on supply demand, and a stalemate in the market price trend. It is expected that the urea market price will continue to fluctuate slightly in the short term.